Q1 earnings season for beverages, alcohol, and tobacco is largely wrapped, and the headline reads better than most expected. Across the 13 companies tracked, revenues beat consensus estimates by 4.9% as a group - a solid showing in a consumer environment that has been anything but predictable. Share prices responded accordingly, rising an average of 7.3% since results came in. But the group average flatters some genuine underperformers, and the spread between the top and bottom of the pack tells the more interesting story.

What ties these companies together isn't just the product category - it's the underlying business pressure they all face: brand loyalty erosion, shifting generational consumption habits, and the constant threat of new entrants who no longer need a massive marketing budget to build an audience. Social media has fundamentally lowered the barrier to brand creation, which means established players can see volume slip to a startup with a clever campaign and a clean label. Operators in adjacent regulated markets - including cannabis retail - know this dynamic well. Point-of-sale data aggregators and retail analytics tools, for instance, help licensed dispensaries track SKU-level demand shifts in ways that larger consumer packaged goods companies are still trying to replicate. Platforms built specifically for regulated retail, like their platform, give operators granular visibility into what's moving and what's stalling - a capability that matters more when consumer preferences move fast.

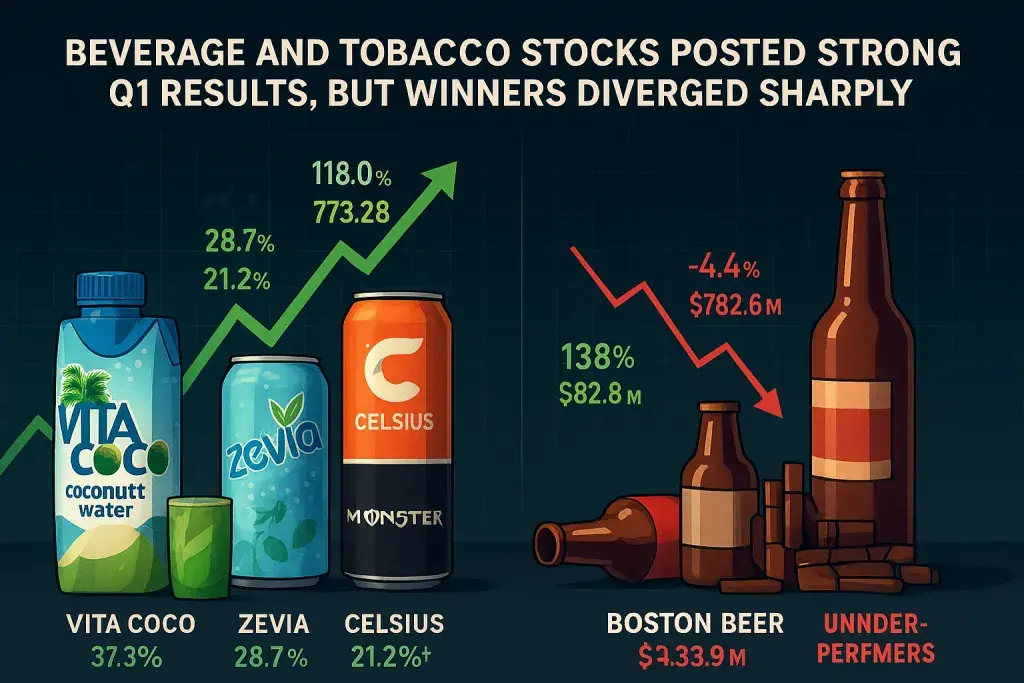

The standout of the quarter was Vita Coco, which reported revenues of $179.8 million - up 37.3% year on year - and beat analyst expectations by 20.5%. That's not a rounding error; that's a company operating materially ahead of where the market thought it would be. Vita Coco also posted the highest full-year guidance raise among its peers, which suggests the outperformance wasn't a one-quarter anomaly. The stock reflected that confidence, rising 41.9% since the report to trade around $73.28. Zevia also had a strong quarter, with revenues of $46.09 million - up 21.2% year on year - beating estimates by 12.2% and posting gains on both EPS and EBITDA. The stock is up 28.7% since reporting. Both companies are selling into the better-for-you consumer trend, and Q1 suggests that trend has real volume behind it, not just marketing rhetoric.

Growth Leaders and the Trends Driving Them

Celsius and Monster deserve separate attention. Celsius reported revenues of $782.6 million, up 138% year on year. That growth rate is exceptional by any measure, and the company topped analyst expectations by 2.6% while delivering beats on EBITDA and EPS. The stock is down 8.6% since reporting, which might seem counterintuitive - but markets were already pricing in extraordinary growth, and a modest beat on those expectations doesn't always move the needle upward. Monster, meanwhile, reported $2.35 billion in revenue, up 26.9% year on year, beating estimates by 9.3%. Its stock is up 26.8%. At that scale, outperforming by that margin reflects strong distribution discipline and brand consistency - harder to sustain than it looks.

The energy drink category, more broadly, has benefited from the same consumer shift away from traditional soda that cannabis retailers understand well. When consumers look for functional or perceived-functional beverages - energy, hydration, wellness - they're drawing from the same attention pool that cannabis-infused beverages are competing for in legal markets. That's a market dynamic licensed cannabis brands and dispensary buyers should be watching. The beverage segment within cannabis retail remains a small but growing SKU category, and the success of mainstream better-for-you drinks signals where consumer appetite is moving.

Where the Quarter Fell Short

Boston Beer is the clearest cautionary case. Revenues came in at $433.9 million, down 4.4% year on year. The company missed adjusted operating income and EPS estimates significantly, and the stock is down 22% since reporting - now trading around $184.97. Boston Beer pioneered craft brewing as a category, but the craft beer segment has fragmented so thoroughly over the past decade that being a pioneer no longer insulates you from volume pressure. The proliferation of small craft labels, the rise of hard seltzer (which Boston Beer itself helped create and then watched cannibalize its own portfolio), and now growing competition from cannabis-adjacent beverages in adult-use markets have all taken a toll. Fair enough to say the company has a brand problem as much as a market problem.

The Boston Beer result is a useful reminder for any brand-reliant business in a regulated market: category creation doesn't confer permanent advantage. Cannabis brands operating in mature markets like California, Colorado, and Oregon are already experiencing version of the same pressure - early brand movers are watching newer, leaner entrants undercut on price and outperform on social media engagement. Vertical integration can provide some insulation, but it doesn't solve a brand relevance problem.

What the Broader Picture Means for Regulated Consumer Markets

The 4.9% revenue beat across the group is a meaningful signal, but the divergence in individual outcomes matters more than the aggregate. Companies that invested in innovation - functional ingredients, cleaner labels, category-adjacent moves - generally outperformed. Those that leaned on legacy brand equity without meaningful product evolution underperformed. That's not a new lesson, but Q1 put a price tag on it.

For cannabis retailers and operators, the parallel holds. Consumer preferences in regulated adult-use markets are not static. The dispensary that treats its product menu as a fixed inventory and its consumer as a guaranteed repeat buyer is running the same risk Boston Beer ran. Demand data at the SKU level, active wholesale menu management, and responsiveness to category shifts - away from flower toward concentrates, beverages, or low-dose formats - are the operational disciplines that separate operators with growing basket sizes from those watching transaction counts decline. The beverage and tobacco sector just illustrated, in public market terms, what those decisions cost over a single quarter.